Start date cannot be after end date.

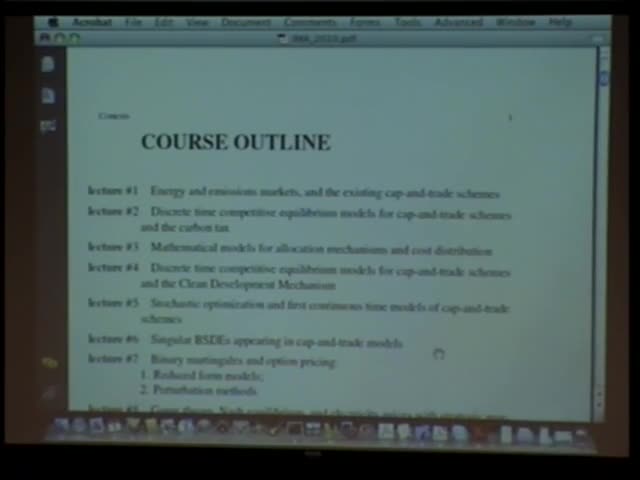

Binary martingales and option pricing: 1) Reduced form models; 2) Perturbation methods

Presenter

- Rene Carmona

June 14, 2010

IMA

Stochastic optimization and first continuous time models of cap-and-trade schemes

Presenter

- Rene Carmona

June 11, 2010

IMA

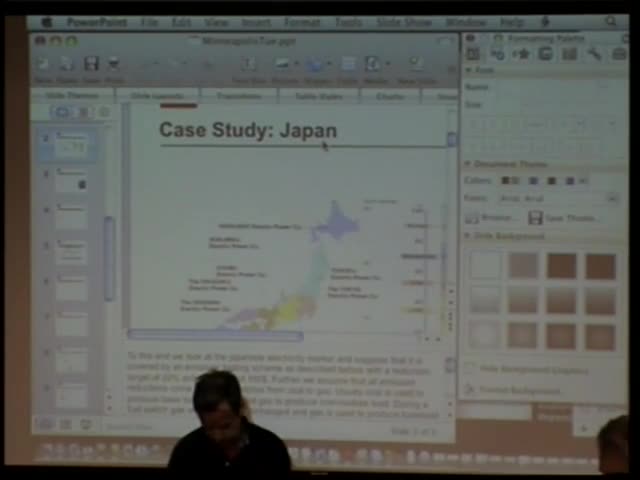

Discrete time competitive equilibrium models for cap-and-trade schemes and the clean development mechanism

Presenter

- Rene Carmona

June 10, 2010

IMA

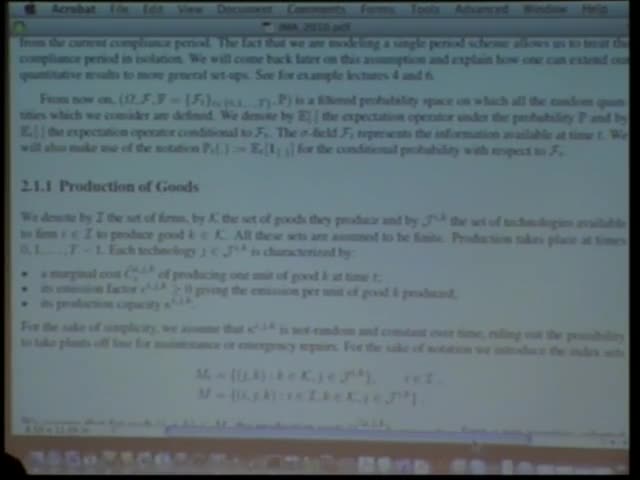

Mathematical models for allocation mechanisms and cost distribution

Presenter

- Rene Carmona

June 9, 2010

IMA

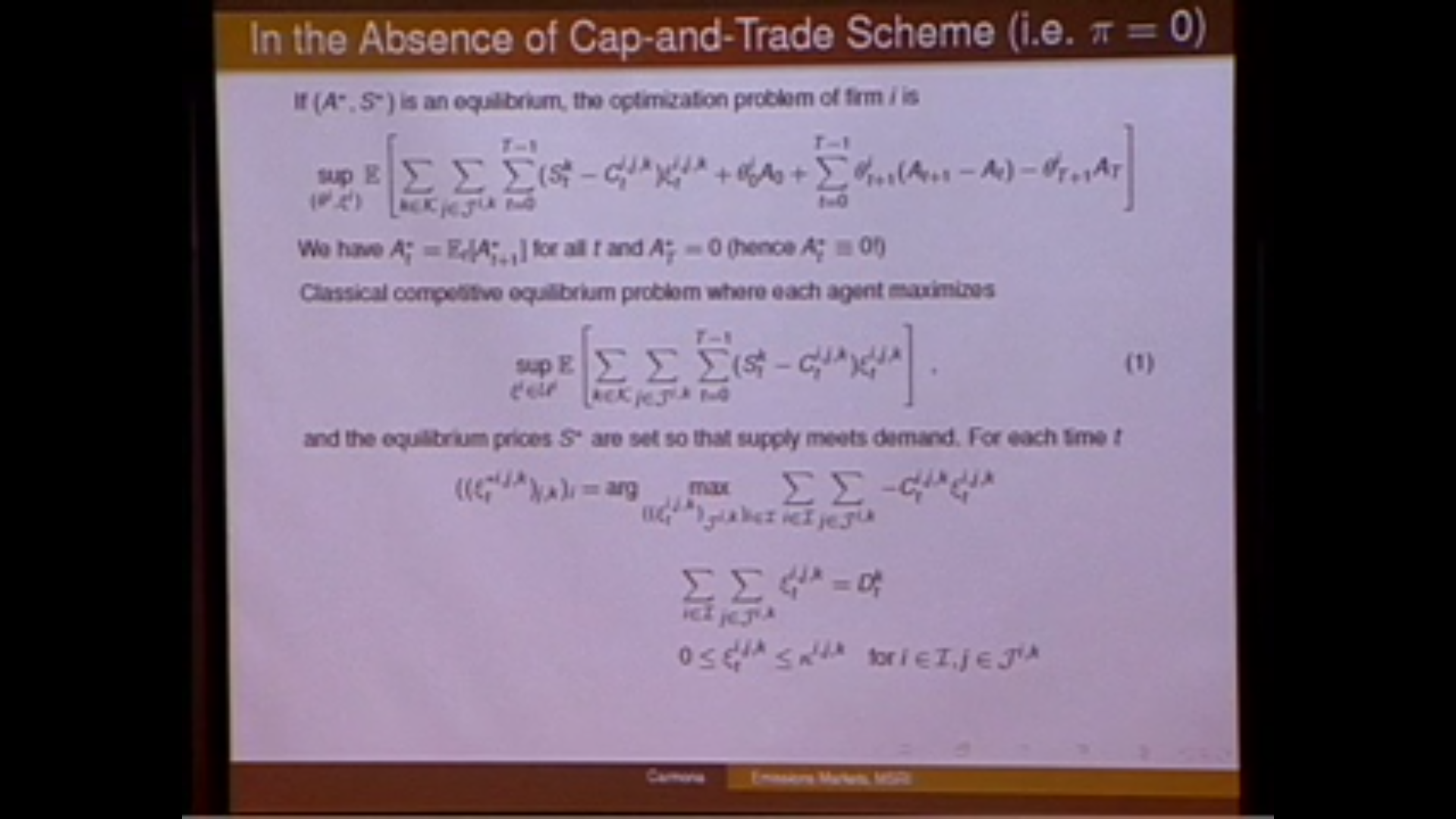

Discrete time competitive equilibrium models for cap-and-trade schemes and the carbon tax

Presenter

- Rene Carmona

June 8, 2010

IMA

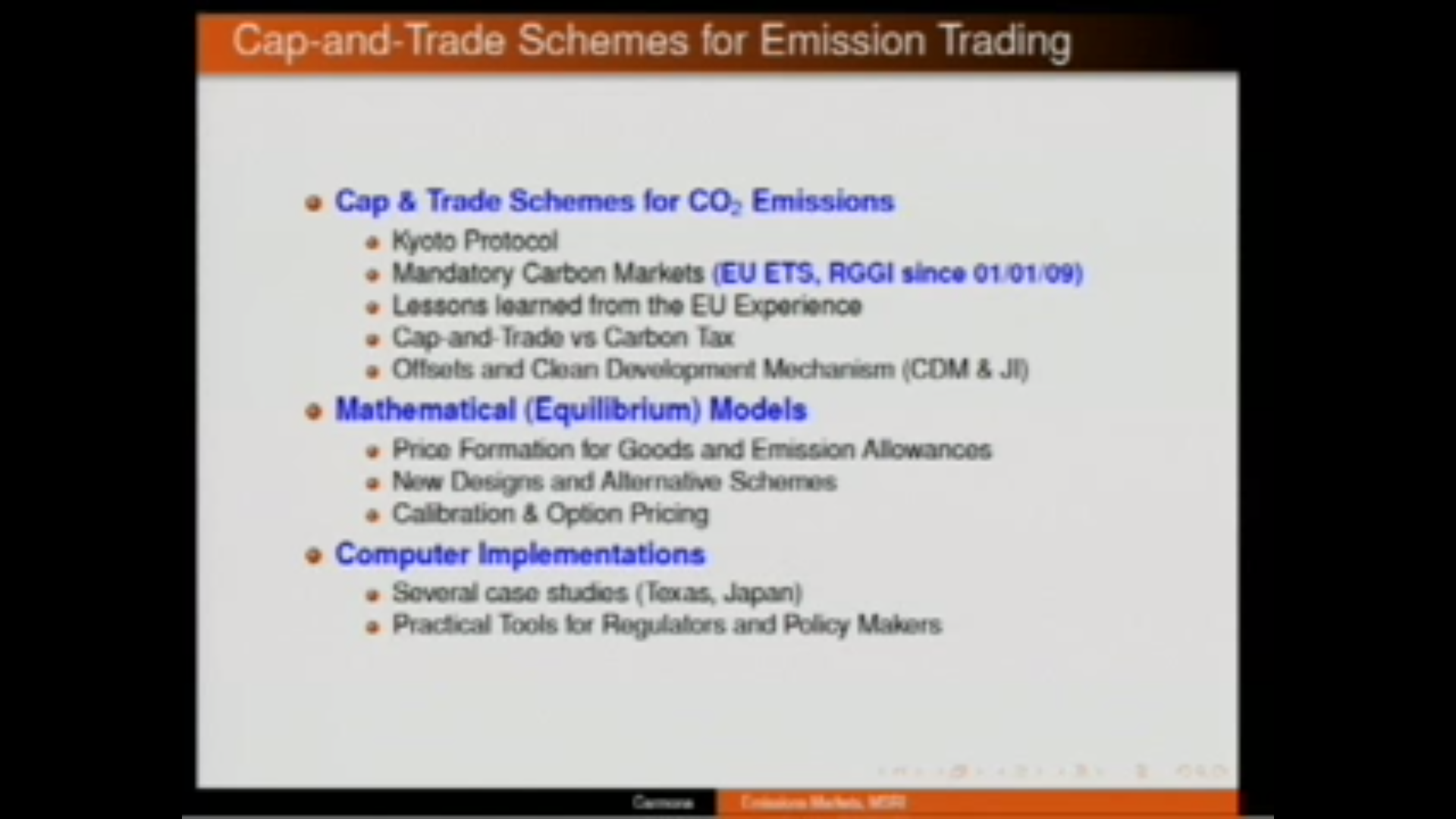

Energy and emissions markets, and the existing cap-and-trade schemes

Presenter

- Rene Carmona

June 7, 2010

IMA

Probabilistic approach to mean field games. An overview.

Presenter

- Francois Delarue

August 28, 2017

IPAM