Start date cannot be after end date.

Workshop on Mathematical Journals, lec. 10 - Everything you did before (and more!) but with a new financial model

Presenter

- James Crowley

February 14, 2011

SLMath

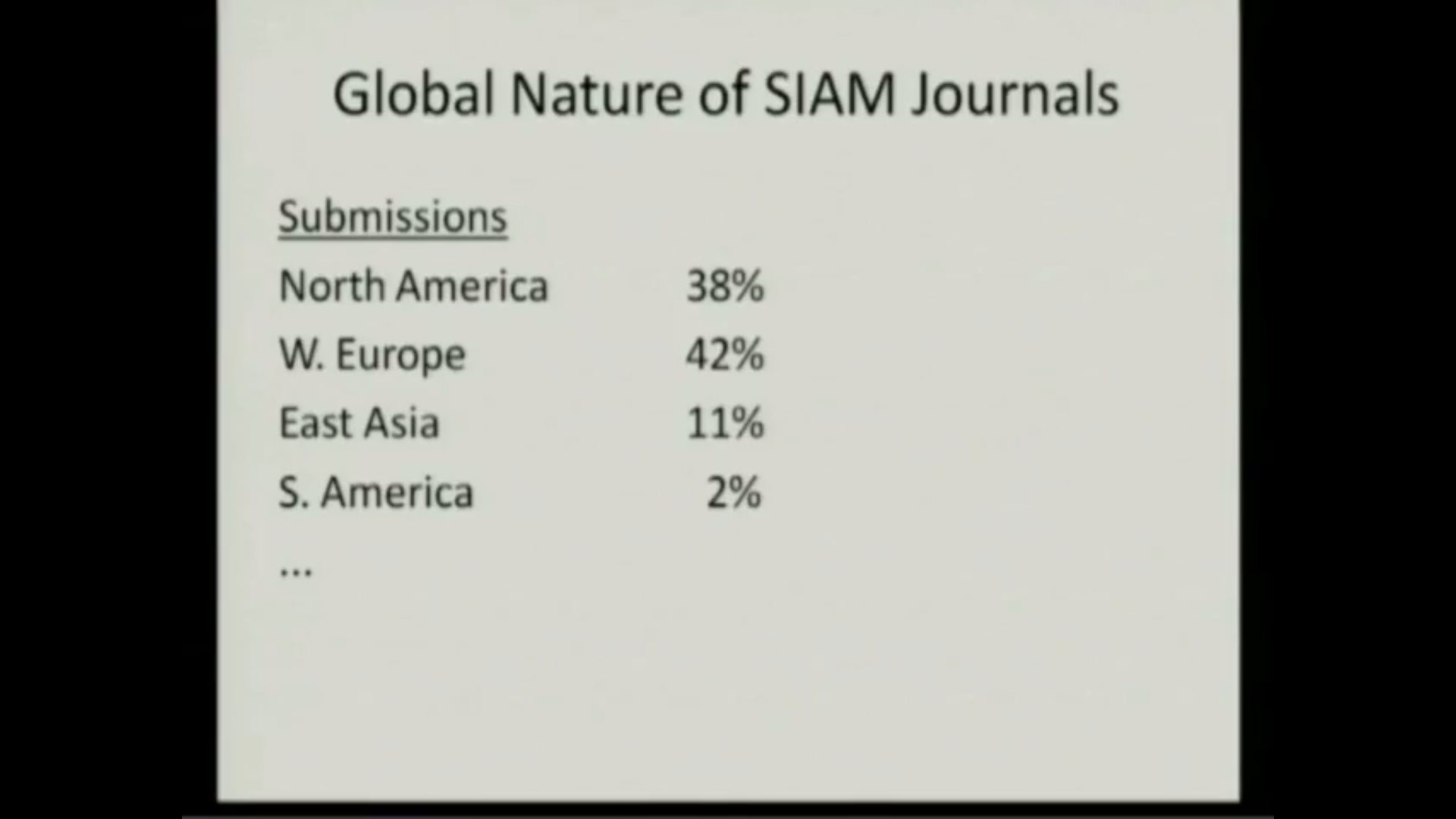

Workshop on Mathematical Journals, lec. 9 - Avenues for Mathematics Journals - on the road to 2025

Presenter

- Samuel Rankin

February 14, 2011

SLMath

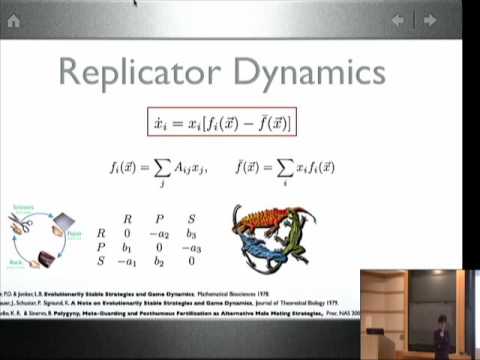

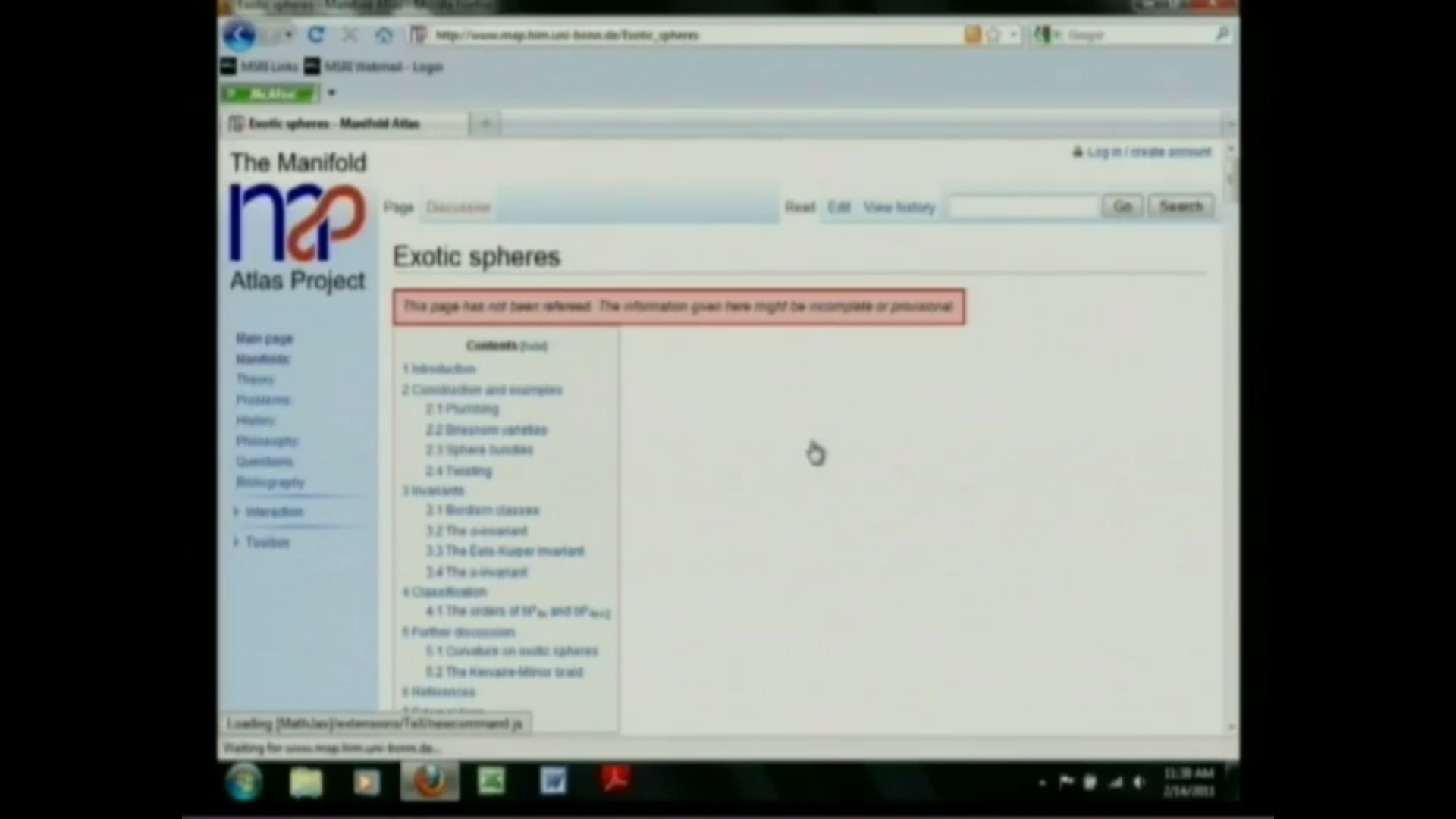

Workshop on Mathematical Journals, lec. 6 - The Manifold Atlas Project - a Model for Future Publishing?

Presenter

- Matthias Kreck

February 14, 2011

SLMath

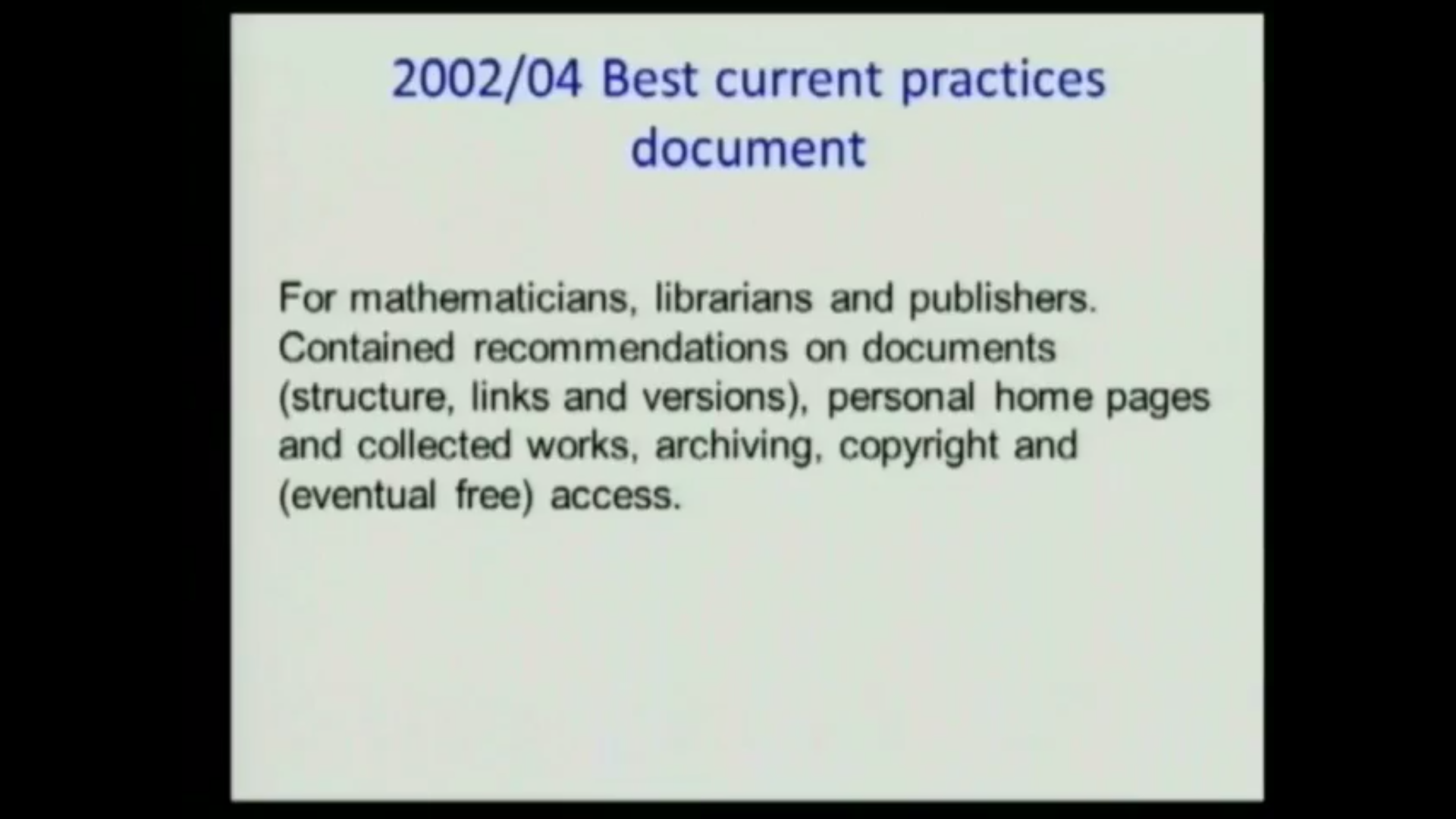

Workshop on Mathematical Journals, lec. 5

Presenter

- Jean-Pierre Bourguignon

February 14, 2011

SLMath

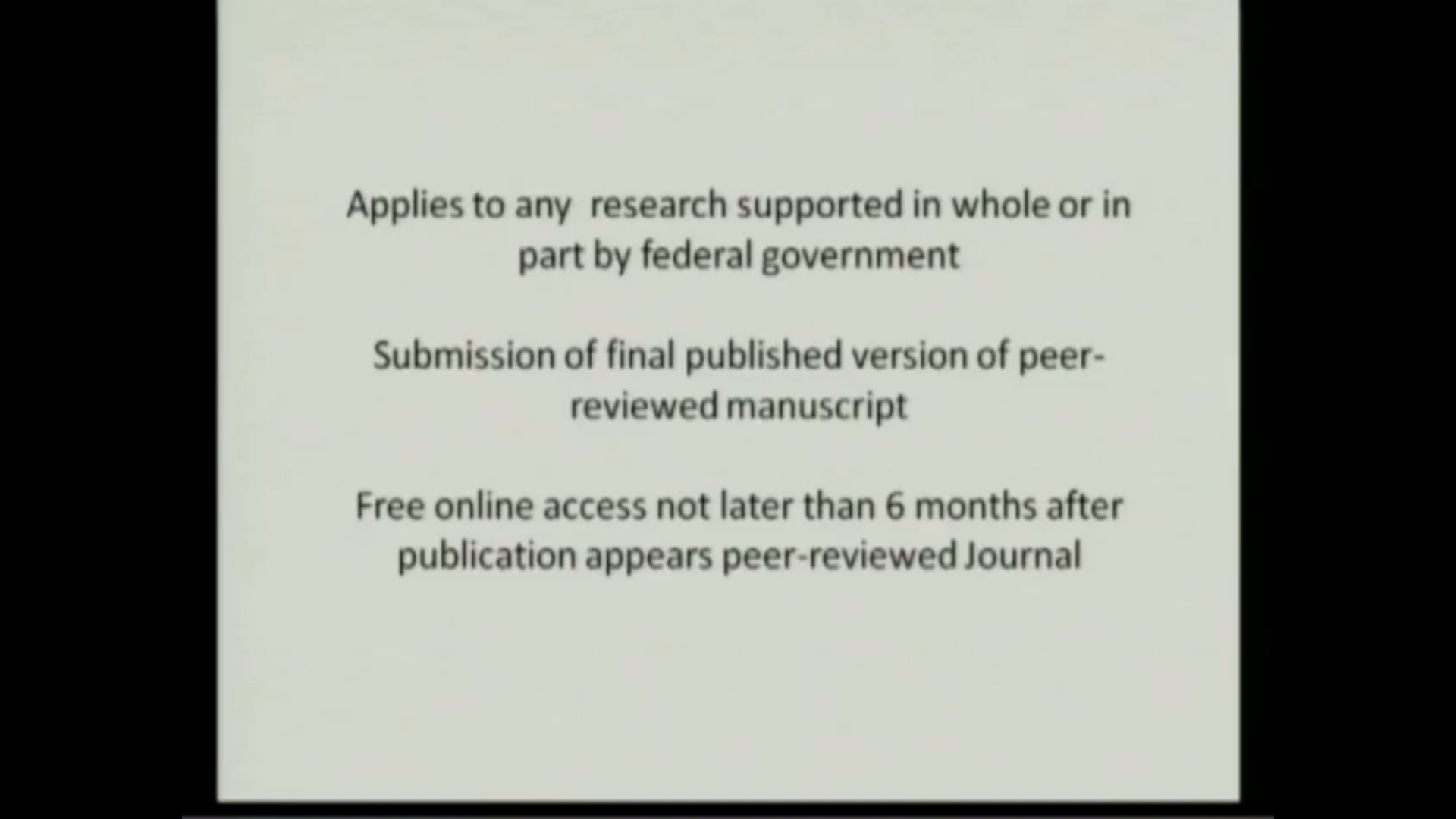

Workshop on Mathematical Journals, lec. 4 - Policymakers and Open Access

Presenter

- Samuel Rankin

February 14, 2011

SLMath

Workshop on Mathematical Journals, lec. 3 - The Work of IMU and CEIC on Journals and Related Issues

Presenter

- John Ball

February 14, 2011

SLMath

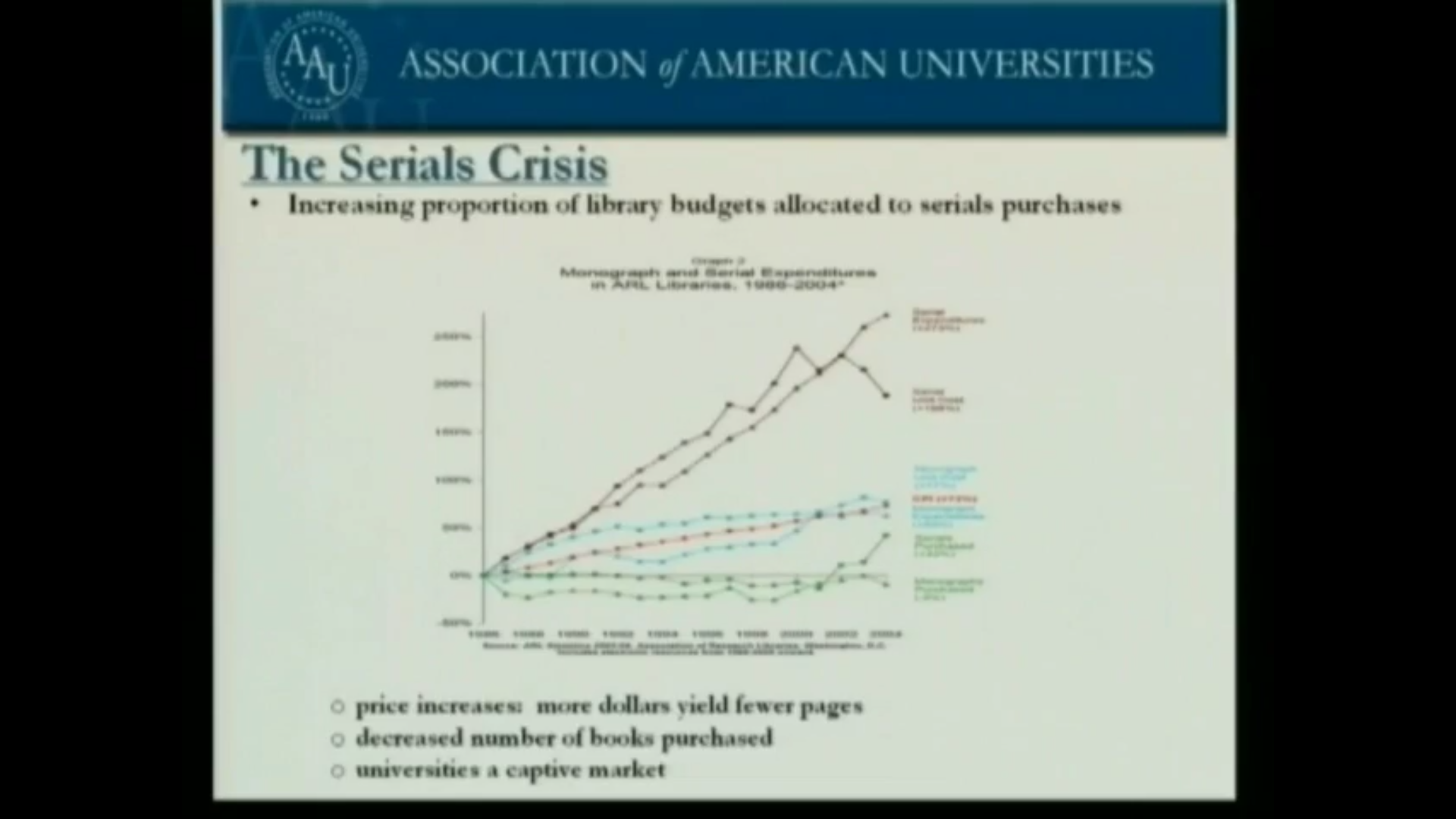

Workshop on Mathematical Journals, lec. 2 - Expanding Public Access to Research Results: Finding a Common Path Forward

Presenter

- John Vaughn

February 14, 2011

SLMath

Workshop on Mathematical Journals, lec. 1 - Introduction - Why are we here and what do we hope to get out of this?

Presenter

- Susan Hezlet

February 14, 2011

SLMath