Efficient Allocations under Ambiguous Model Uncertainty

Presenter

May 3, 2022

Abstract

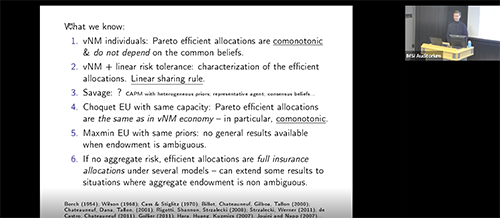

We investigate consequences of ambiguity on ex ante efficient allocations inan exchange economy. The ambiguity we consider is embodied in the modeluncertainty perceived by the decision maker: they are unsure what would bethe appropriate probability measure to apply to evaluate consumptioncontingent on a state space and keep in consideration a set P of alternative probabilistic laws p. We study the case wherethe typical consumer in the economy is ambiguity averse with smoothambiguity preferences (Klibanoff et al. (2005) and P is point identified, i.e., the true law p in P can be recoveredempirically from events, a framework axiomatized in Denti and Pomatto (2021). Differently from the literature, we allow for the case wherethe aggregate risk is ambiguous and agents are heterogeneously ambiguityaverse. Our analysis addresses, in particular, the full range of set-upswhere under expected utility the Pareto efficient consumption sharing ruleis a linear function of the aggregate endowment. We identify systematicdifferences ambiguity aversion introduces to optimal sharing arrangements inthese environments and also characterize the representative consumer.Furthermore, we investigate the implications for the state-price function,in particular, the effect of heterogeneity in ambiguity aversion.