An Improved Cutting Plane Method for Convex Optimization, Convex-Concave Games and its Applications

Presenter

March 2, 2020

Abstract

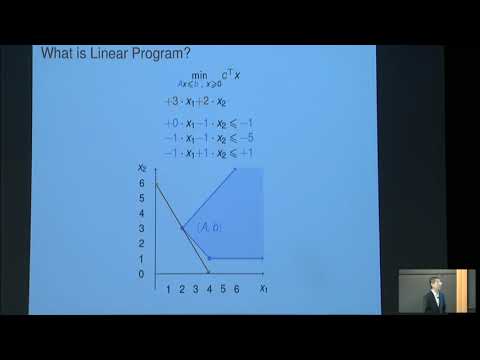

Given a separation oracle for a convex set $K \subset \mathbb{R}^n$ that is contained in a box of radius $R$, the goal is to either compute a point in $K$ or prove that $K$ does not contain a ball of radius $\epsilon$. We propose a new cutting plane algorithm that uses an optimal $O(n \log (\kappa))$ evaluations of the oracle and an additional $O(n^2)$ time per evaluation, where $\kappa = nR/\epsilon$.

This improves upon Vaidya's $O( \text{SO} \cdot n \log (\kappa) + n^{\omega+1} \log (\kappa))$ time algorithm [Vaidya, FOCS 1989a] in terms of polynomial dependence on $n$, where $\omega < 2.373$ is the exponent of matrix multiplication and $\text{SO}$ is the time for oracle evaluation.

This improves upon Lee-Sidford-Wong's $O( \text{SO} \cdot n \log (\kappa) + n^3 \log^{O(1)} (\kappa))$ time algorithm [Lee, Sidford and Wong, FOCS 2015] in terms of dependence on $\kappa$.

For many important applications in economics, $\kappa = \Omega(\exp(n))$ and this leads to a significant difference between $\log(\kappa)$ and poly$(\log (\kappa))$. We also provide evidence that the $n^2$ time per evaluation cannot be improved and thus our running time is optimal.A bottleneck of previous cutting plane methods is to compute leverage scores, a measure of the relative importance of past constraints.Our result is achieved by a novel multi-layered data structure for leverage score maintenance, which is a sophisticated combination of diverse techniques such as random projection, batched low-rank update, inverse maintenance, polynomial interpolation, and fast rectangular matrix multiplication. Interestingly, our method requires a combination of different fast rectangular matrix multiplication algorithms. Our algorithm not only works for the classical convex optimization setting, but also generalizes to convex-concave games. We apply our algorithm to improve the runtimes of many interesting problems, e.g., Linear Arrow-Debreu Markets, Fisher Markets, and Walrasian equilibrium.

This is a joint work with Haotian Jiang, Yin Tat Lee, and Sam Chiu-wai Wong