Optimal Asset Allocation with Stochastic Interest Rates in Regime-Switching Models

Presenter

June 15, 2018

Keywords:

- Optimal asset allocation, portfolio optimization, stochastic control, regime-switching models, stochastic interest rate, power utility.

Abstract

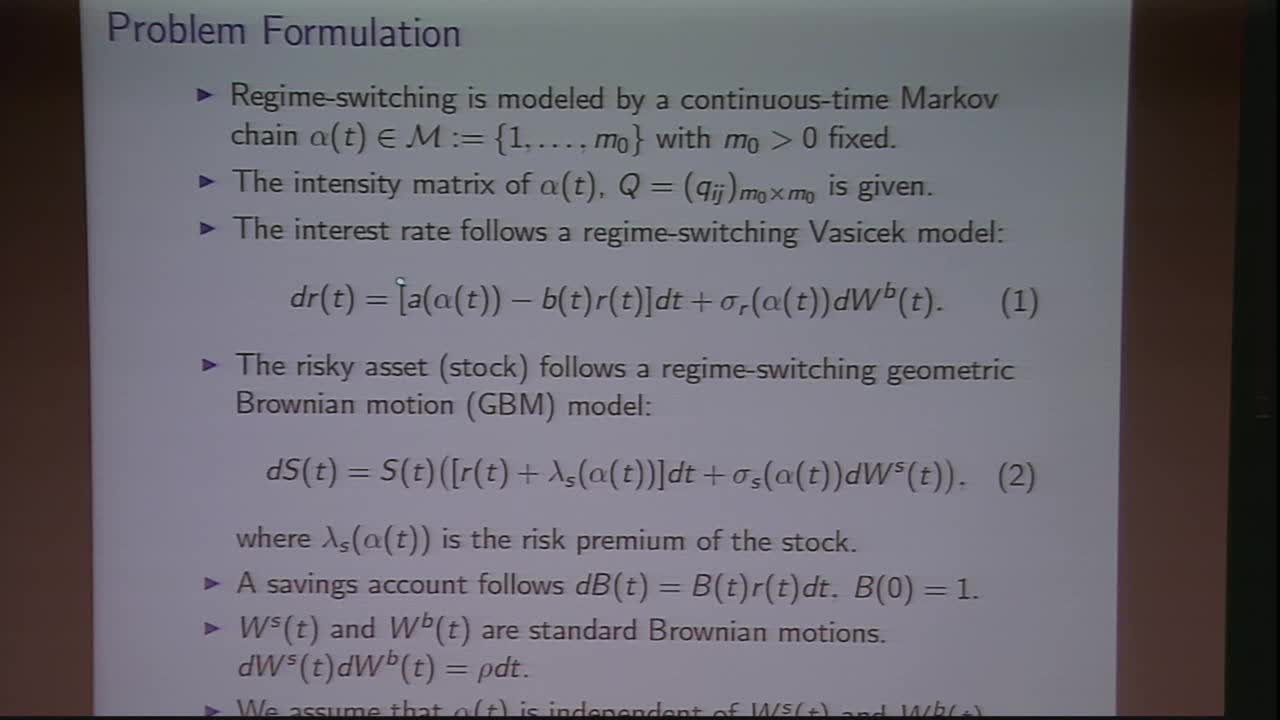

In this talk we present some results on optimal asset allocation with stochastic interest rates in regime-switching models. A class of stochastic optimal control problems with Markovian regime-switching is formulated for which a verification theorem is provided. The theory is applied to solve two portfolio optimization problems (a portfolio of stock and savings account and a portfolio of mixed stock, bond and savings account) while a regime-switching Vasicek model is assumed for the interest rate. Closed-form solutions are obtained for a regime-switching power utility function. Numerical results are provided to illustrate the impact of regime-switching on the optimal investment decisions.

This talk is based on the joint works with Cheng Ye and Dan Ren.